Why a house-property tax shouldn't be introduced next year

There is a strong argument that the Government should not introduce a house-property tax next year: the economy and hundreds of thousands of households simply cannot absorb it. By Michael Taft.

Let’s assume the Government comes up with the best house-property tax ever devised – truly progressive, taking into account all the social factors such as unemployment, low-income, arrears, and mortgage equity (or lack of). Yes, it’s a big assumption but let’s try it anyway. If this occurred there is still a strong argument that the Government should not introduce such a tax next year or even the following. And that is because the economy and hundreds of thousands of households cannot absorb it. Let’s run through some of the arguments.

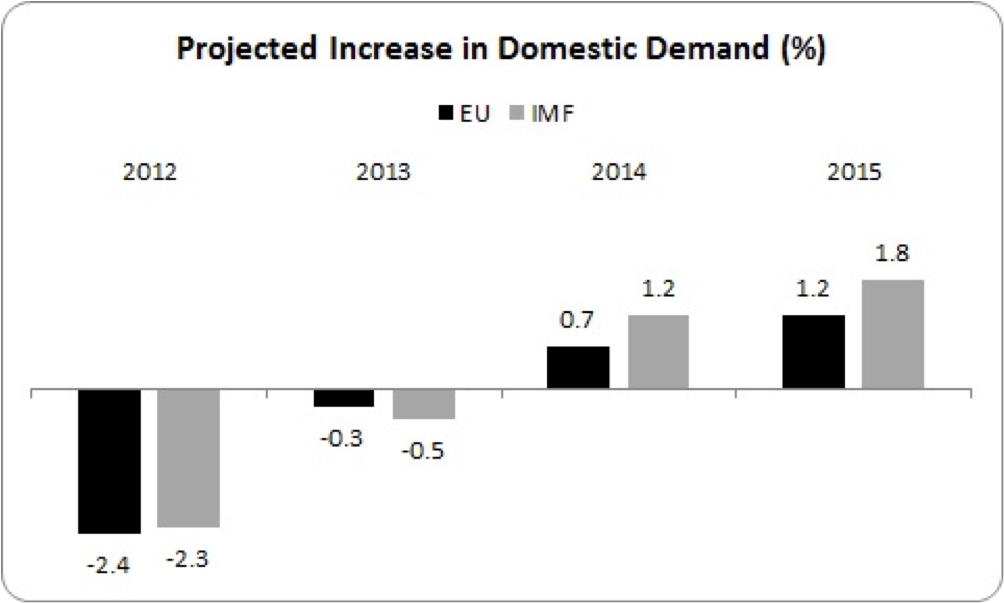

First, the domestic-demand recession is expected to continue next year – the sixth year in a row.

As seen, both the EU and the IMF expect domestic demand (consumer spending, government spending on public services, and investment) to fall again next year. They both estimate that consumer spending will fall, as more people wilt under the combination of austerity measures, falling incomes and unemployment. Even by 2014, domestic demand will start rising, but only marginally.

As seen, both the EU and the IMF expect domestic demand (consumer spending, government spending on public services, and investment) to fall again next year. They both estimate that consumer spending will fall, as more people wilt under the combination of austerity measures, falling incomes and unemployment. Even by 2014, domestic demand will start rising, but only marginally.

While under normal growth conditions, a house property tax would be an efficient tax – limited impact on the domestic economy and more efficient at reducing the deficit; relative to spending cuts. Even so, the impact on consumer spending would be high: for every €100 raised in a house-property tax, there is a resulting reduction of approximately €75 in consumer spending. In normal growth situations, the economy would absorb this. But as we know, these are not normal times. So what would be the impact of introducing such a tax while the economy is still in a domestic-demand recession?

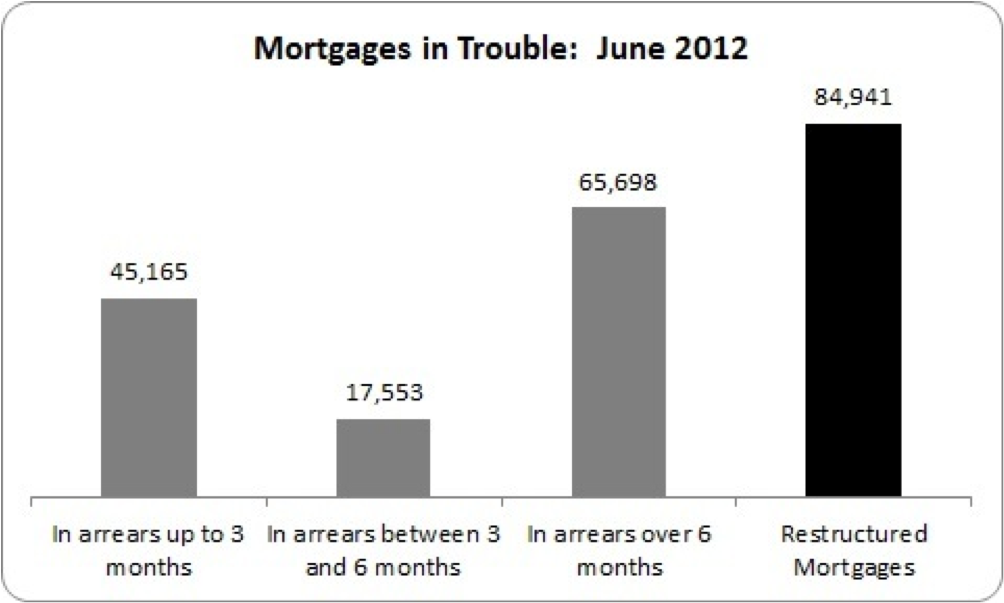

Second, what would the impact of such a tax be on mortgages in trouble? The Central Bank reports the following:

In June, 28% of all mortgages were in arrears or were restructured (interest payments only, reduced payment, payment moratorium, etc.). That comes to 213,000 mortgages. Even more worrying, 34% of the value of all mortgages is either in arrears or has been restructured.

In June, 28% of all mortgages were in arrears or were restructured (interest payments only, reduced payment, payment moratorium, etc.). That comes to 213,000 mortgages. Even more worrying, 34% of the value of all mortgages is either in arrears or has been restructured.

This picture is getting worse. Back in September last year there were 183,000 in arrears or restructured. There has been an increase of 16% in troubled mortgages in the last nine months. And there is no sign that the trend has topped out.

Question: is it a smart idea to introduce a house-property tax with so many mortgages in trouble?

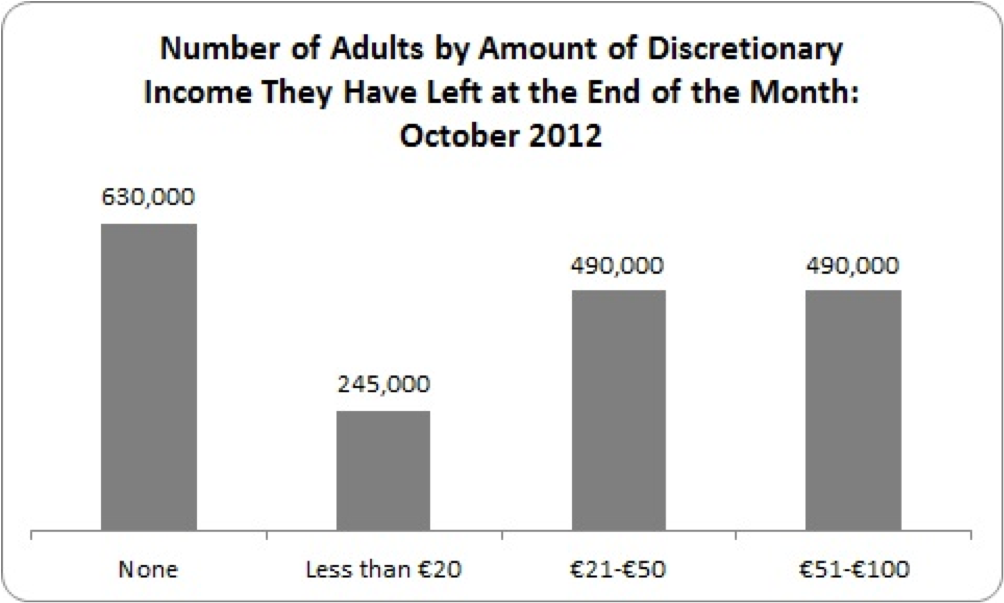

Third, the League of Credit Union’s What’s Left Tracker shows the low and ultra-low level of discretionary income people have at the end of the month – that is, what’s left after tax and essential bills. The numbers are staggering.

1.9 million – over half – have less than €100 at the end of the month. Though not everyone in this category will own a house (such as public and private rented tenants) there will be a sizeable proportion who will be subject to a house-property tax if it is implemented. And though this is a subjective measurement (it is left to people to determine what an essential bill is), what is worrying is that this number – 1.9 million – has increased by over 50,000 in just three months. It is a strong indicator of the high number of people on the edge.

1.9 million – over half – have less than €100 at the end of the month. Though not everyone in this category will own a house (such as public and private rented tenants) there will be a sizeable proportion who will be subject to a house-property tax if it is implemented. And though this is a subjective measurement (it is left to people to determine what an essential bill is), what is worrying is that this number – 1.9 million – has increased by over 50,000 in just three months. It is a strong indicator of the high number of people on the edge.

Fourth, real wages are projected to fall next year. The EU projects that wages (employee compensation) will fall by 1.3% after inflation. The IMF and the Government are less pessimistic – projecting falls of -0.2 and -0.3 respectively. The ESRI projects a real wage fall of -1.8%, using the Consumer Price Index. Whichever is more prescient, they all agree – wages will fall after inflation. With living standards falling, what will the impact be of introducing a new layer of taxation?

What we have left is a grim set of indicators of continuing recession, growing arrears and falling income. It is questionable how much more the economy can take – never mind the people who populate that economy.

There will be the claim that the Government has to get money from somewhere. Yes, of course, but here is the problem – if you introduce new taxation measures on a depressed economy and an even more depressed society, you won’t get the money, whatever the budget line promises. For the extra taxation results in people reducing their spending; businesses react to falling turnover by squeezing their payroll through cutting wages, working hours and even employment. This, in turn, leads to depressed tax revenue and higher public spending if there are job losses. And, so, the deflationary cycle continues its downward slope.

None of this argues against the principle of a house-property tax, only its timing (though I hold heretical, minority thoughts on the subject: houses, when consumed as homes, should be exempt from recurring taxes; houses, when used for a capital gain or income, should be taxed appropriately – but I accept this will probably not get much traction).

Of course, there is the issue of the design of the tax – will the Government tax all property - housing and financial? If it excludes the latter it will be giving a substantial subsidy to high-income groups. Will the house-property tax be progressive? And how will we know if they don’t measure the income-distribution impact (don’t hold your breath). How will it treat low-income earners, unemployed, those in arrears, etc?

The point in this post, however, is the fiscal timing during a period of stagnation. In the medium-term taxation will have to increase (and Donagh Brennan poses this issue with clarity). But smart fiscal consolidation lays down a few principles. Before taxation rises we must first return to reasonable growth – employment and real wages. This will broaden the tax base and make it easier for households to absorb the increase without a negative impact on consumer spending. Before taxing houses, we can add another principle – we need a substantial write-down of mortgage debt. Otherwise, we will be taxing arrears and debt, rather than equity.

So where do we get the money in the short-term, while introducing measures to lay the foundations of growth and debt write-down? The Minister for Finance provided the answer to the Dáil:

“The Deputy (Seamus Healy) referred to the wealth tax in France, which is at 1.5%. On a pro rata basis, that kind of tax in Ireland would have a yield of €400 to €500 million per annum.”

Hmmm. Here is a property tax, a comprehensive property tax, which includes both housing and financial property, a tax that would have minimal impact on domestic demand as it would hit only a tiny proportion of households, a tax that would raise up to €500 million. That’s the same amount the Government has said it wants to raise from a house-property tax.

Isn’t it time to pursue smart fiscal consolidation?

Image top: Images_Of_Money.