What to do with the windfall

Investing the €800 million saved through the interest rate cut on Ireland's bailout loan, and dispensing with spending cuts, would provide a real boost to the economy. But the Government may avoid such an approach for political rather than economic reasons. By Michael Taft.

What a government does with an unexpected windfall says as much about its economic priorities as what it does when faced with a cash shortage. Whether the interest rate cut was the result of the Government’s negotiating skills or just a by-product of the EU’s attempt to prevent Greece from crashing and taking Italy with it, the Government has a substantial windfall which could amount to €4 billion over the next four years. So what are we going to do with it?

If the Government has confidence in its own budgetary projection, it does not need the interest rate savings to reach the Maastricht deficit target under the EU-IMF deal. Currently, they are projecting the deficit will be 2.8% by 2015 – hitting the target by a comfortable margin. If they pocket it and continue with the current strategy, the deficit will fall to 2.4%. This is wholly unnecessary.

This, therefore, opens up the question as to what is the best use that can be made of this money. Minister for Finance Michael Noonan was quick to state his determination to continue with spending cuts. But why? This is not in keeping with his statement to the Dáil, in which he set out his fiscal formula: namely, that budgetary measures can be substituted as long as the deficit reduction impact remains the same.

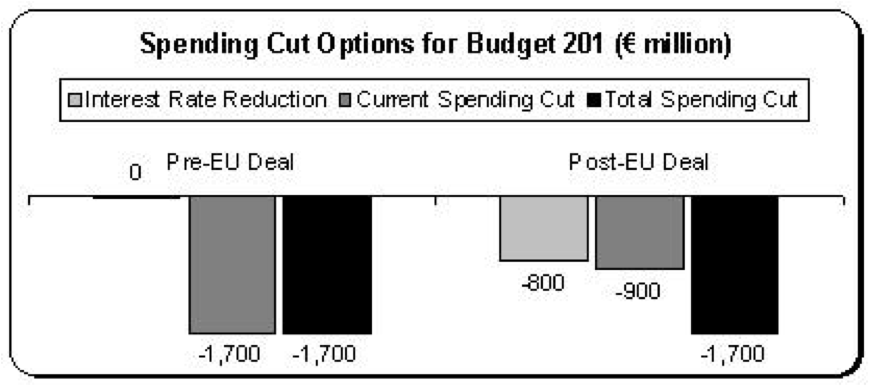

There are two uses of the interest rate reduction that would enhance growth and employment, and hence cut the deficit even more under the current Government strategy. For the purposes of these examples, we will assume an €800 million interest rate cut windfall in 2012.

Take the Foot Off

In this approach, the Government could take the foot off the austerity pedal. This is always a benefit – especially as austerity is highly damaging to the economy while doing little to cut the deficit.

The Government intends to introduce a fiscal consolidation package of €3.6 billion, made up of €2.1 billion in spending cuts (of which €1.7 billion is current spending cuts) and €1.5 billion in tax increases. With the lower interest rate, only €900 million need be cut.

There will be some commentators who will cry that we are avoiding the “necessary cuts, the necessary pain”. What would happen, however, is just the opposite. Based on the Minister for Finance’s own calculation, reducing the non-interest cuts would boost GDP by a minimum of €500 million, or a third of one percent, while increasing tax revenue by over €100 million. Pretty good result for not doing the wrong thing – namely, cutting spending.

Start the Investment Drive

A second option – and one that I would favour – is to use the windfall to part-fund a substantial investment programme. Nick Webb, Business Editor of the Sunday Independent, supports this approach; in proposing "10 smart ideas to stimulate the economy". One doesn’t have to agree with all his ideas, but his premise is certainly worthy of support:

‘ . . . we still need something to kick-start the economy. You can't grow by cutting. And we can't get out of the debt crisis without growing the economy. We need our own Marshall Plan, part- funded by the €800m savings in the bailout interest rate, to stimulate growth again unless we want to face a ‘lost decade’ of joblessness and zero opportunities.’

If the €800 million, rather than relieving the projected spending cuts, was invested through the capital budget, the economy would receive a real boost:

- GDP would rise by nearly €1 billion , or 0.6%

- Tax revenue would rise by over €300 million

- Direct employment would rise by approximately 10,000 with indirect employment increasing by over 3,000

- The increase in employment would mean lower public spending, through people coming off the dole

It is a real win-win-win all around: higher growth, lower deficit and higher employment.

In actual fact you could merge the two – for the Minister for Finance’s fiscal formula shows that public spending cuts are a political choice, not something required by the EU-IMF deal. So we could dispense with spending cuts altogether – providing one boost – while taking the €800 million in the reduced interest rate and investing it – providing an additional boost.

This is the choice the Government has – if they are not locked-down ideologically. Or if they actually have no confidence in the budgetary projections they produced only a few weeks ago - that the deficit is refusing to budge, and that they need the €800 million in a frantic scramble to reach fiscal targets which were never going to be reached under the current strategy.

If so, the Government should make this clear. Because there is an alternative now on the table, courtesy of Greece or Italy or whomever.

{jathumbnailoff}