Wealth - now you don't see it, now you do

There is plenty of wealth in Ireland, more than in most European countries, in fact. By Michael Taft.

The issue of wealth in Ireland is certainly hotting up – at least in the Irish Times. Last week we had a strong intervention by Fintan O’Toole, claiming that Ireland is an extremely wealth country, a fact that contradicts the austerity narrative we are being subject to.

A few days later Dan O’Brien claimed that Ireland was never wealthy and Irish wealth lags behind western European peers. So who are we to believe?

When you go to the data, the striking thing is that, per Fintan, Ireland has one of the highest levels of financial wealth per capita in the EU; and even higher levels of wealth per adult.

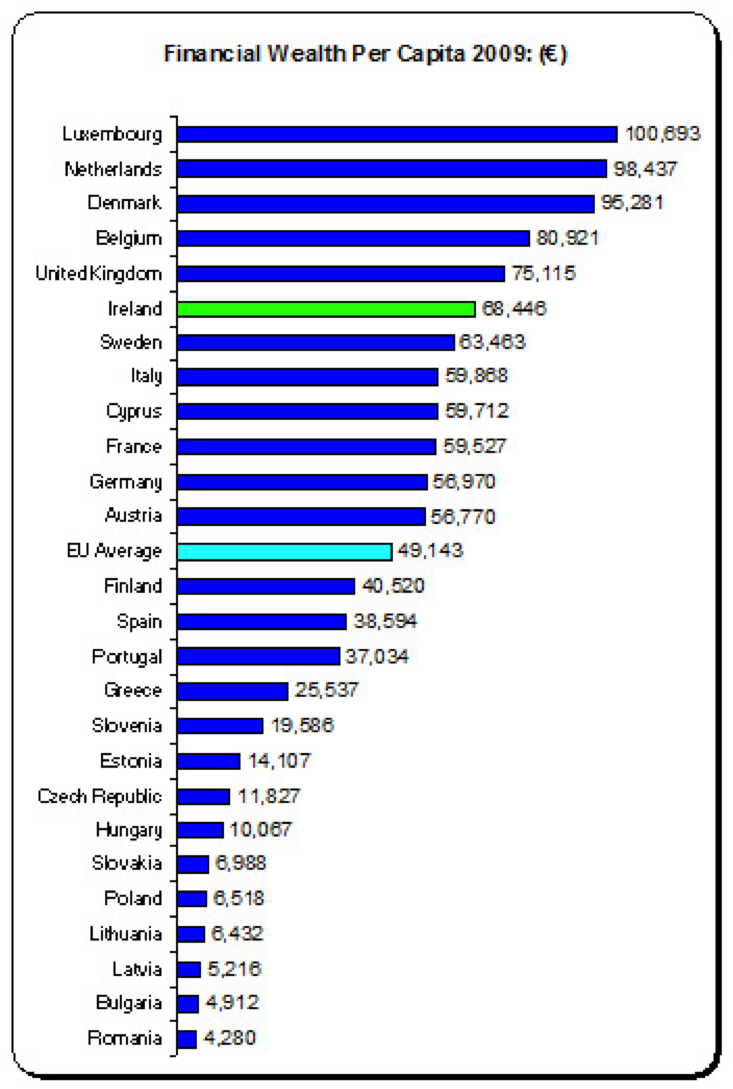

Financial wealth is made up of primarily cash, shares & equity, and pension/insurance funds. It does not include housing or land. It does not measure income. The Eurostat data which Dan refers to can be found here, compiled by the members-states’ data agencies. In Ireland, the CSO collects this data, which can be found here. Let’s first look at the total financial wealth per capita – the total amount of cash, shares, equity, etc. held by each man, woman and child (it is, of course, an average).

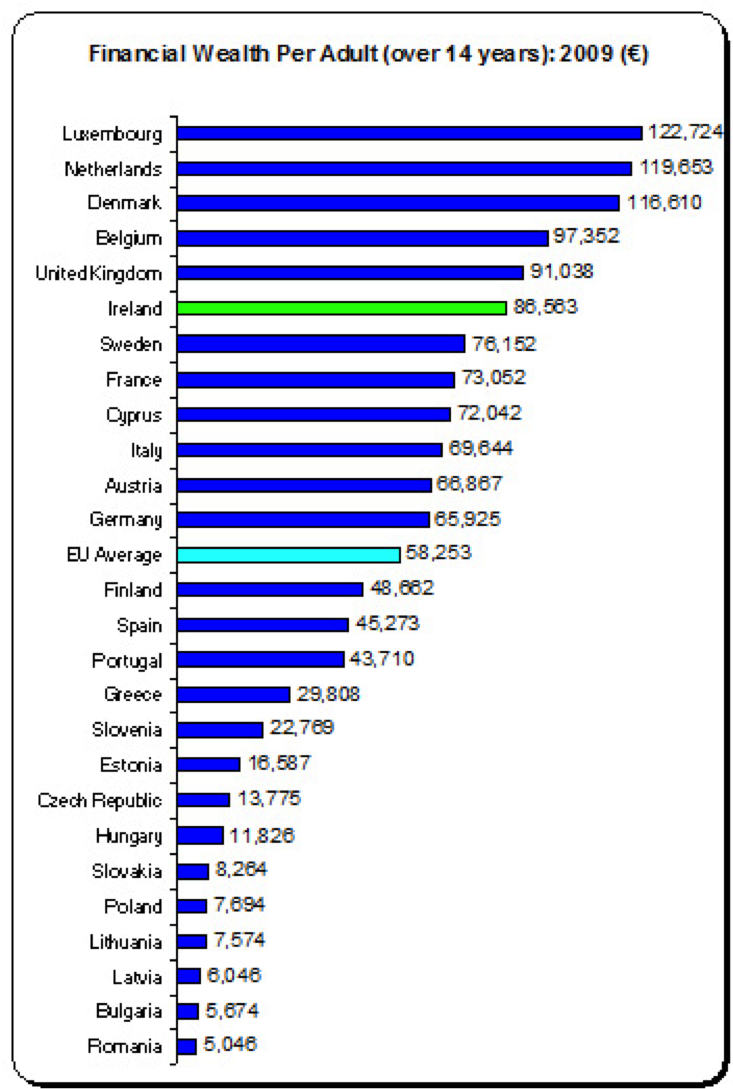

Ireland is at the wealthier end of EU table – sixth out of 27 countries and nearly 40% above the EU average. Of course, using per capita is a bit off the mark. After all, children don’t own wealth. So when we adjust for populations excluding those under 15 years, what does the wealth-per-adult table tell us?

Ireland is still in sixth place, but now we jump to 50% above the EU average. Each Irish adult owns, on average, over €86,000 in cash, share and/or pension fund equity - €30,000 more than the average EU adult. How has this changed over time?

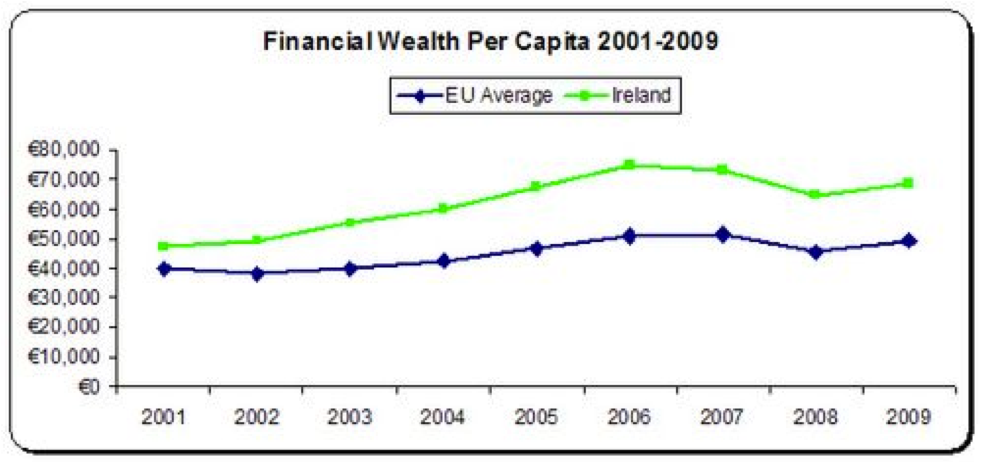

Irish wealth has been growing and the gap between the EU average has been widening. In 2001, Irish wealth per capita was €7,403 higher than the EU average. This climbed to €24,188 by 2006. It fell back over 2007 and 2008, but Irish wealth started growing again in 2009 – widening the gap once more with the EU average. Now let’s look at some of the constituent elements of wealth: cash, shares, equity, etc.

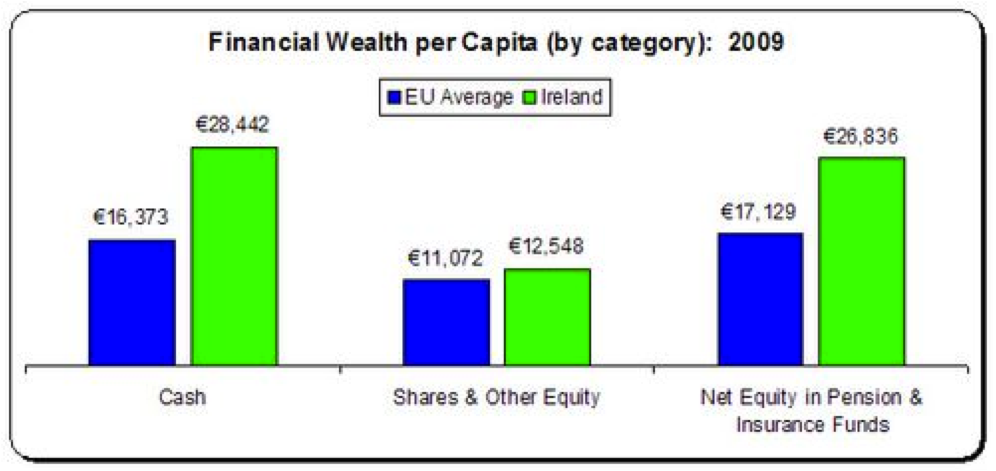

Irish wealth is more concentrated in cash and pension/insurance funds – though we still own more shares and equity than the European average.

So taking all of the above, it seems Fintan nailed it – there is plenty of wealth in Ireland, more than in most European countries. This is confirmed by the Allianz Global Wealth report, which puts Ireland in the upper half of not only European but OECD countries as well (the relevant table is on page 81).

And in 2009, when the economy was tanking, when people were losing their jobs and the Government was hammering everyone with three austerity budgets – Irish financial wealth increased by €21 billion, or 7%, recovering most of the ground that was lost since 2007.

Given this, how can Dan O’Brien claim that Ireland is not wealthy – that we are similar to Greece, Estonia and Slovenia? That’s because Dan looks at ‘net financial assets’ – that is, the amount of financial wealth left after you subtract financial liabilities. To be fair to Dan, this is ‘a’ standard measurement. And he at least acknowledges that his claim is based on this measure alone (‘By this measure, Ireland was never wealthy’). Then he takes this result and sets it against GDP.

But there are three major problems with this particular formulation.

First, wealth is exclusive - financial wealth particularly so. Different studies can be found to show that the top 1% of households hold anything from 25% (in Spain) to 42% (in the US) of financial wealth. The Bank of Ireland Private Banking uses estimates from the UK which project that the top 1% own 33% of all financial wealth. There are no contemporary studies in Ireland.

Let’s run with the UK measure: if the top 1% of households own a third of all the financial wealth in Ireland what does that mean?

- Approximately 20,000 households own €100.8 billion (billion, not million)

That’s exclusive. It’s so exclusive it’s hard to get one’s head around those numbers.

But if wealth is concentrated, debt is democratic. Financial liabilities refers mostly to ‘loans’ and in the Irish context, mortgages. We don’t have a distributional breakdown (that is, liabilities broken down by deciles). But it’s reasonable to assume that mortgage debts are spread much more evenly among the populace than share holdings.

To set mortgage debt off against financial assets is to mix apples and oranges. Mortgage debt should be set off against housing assets, not financial assets. This debt does not arise, for the most part, to purchase a financial asset but rather a house. That is why it shouldn’t even be called a ‘financial liability’ but rather a ‘housing liability’ – where it has been borrowed for the purposes of obtaining a home.

Lastly, using ‘net assets’ can lead us to absurd conclusions. Assets are something owned today, liabilities are debts paid out of future income. If I have €100,000 in cash and another €100,000 in shares while paying off a €220,000 mortgage – I’m ‘net asset’ poor on paper; my liabilities exceed my assets. But that is on paper; in real life – as long as I have a good income (and with €200,000 in cash and shares I probably do) - every year I will be reducing my liabilities (that is, paying off my mortgage) while seeing my cash earn interest and my shares appreciate.

On the other hand, if I have no cash, no shares, no assets and no job but a liability of €20,000, I’m on paper no worse than the example above (in net terms); but in fact I’m really up the creek.

It is unfortunate we don’t have a distributional analysis of all this. It is unfortunate we don’t have a thorough analysis of wealth holdings in this country (in other jurisdictions, asset holdings feature as part of the census). But it is unlikely the Government will make any moves to conduct an official analysis – for this would reveal an unpalatable fact and force them to come up with, for them, an ideologically uncomfortable response.

Namely, that a tax on financial assets (actually, it’s a property tax – a tax on financial property) is both an economic necessity and a moral imperative.

And another benefit of such an analysis would be that we wouldn’t have to suffer claims that we are somehow ‘financially poor’.

After all – if you’re one of those 20,000 households which own €100 billion, the holes in your shoes are just a fashion statement.

notesonthefront.typepad.com

Image top: DavidDMuir.

{jathumbnailoff}