Technical recession on Lollipop Lane

We need less talk about "marching toward recovery" and more acknowledgement that we have a way to go before domestic demand bottoms out. By Michael Taft.

The headline reads: ‘GDP rises for first time in four years’. Well, that’s good news. The report goes on:

“The Irish economy grew in 2011...according to figures released yesterday by the Central Statistics Office. This was the first time since 2007 that GDP grew over the course of a full year. GDP in 2011 was 0.7 per cent higher than in 2010. This was half the average rate recorded across the euro area as a whole, where GDP growth stood at 1.4 per cent. The Irish rate of growth was higher than the weaker southern European economies, but well below the stronger economies of northern Europe.”

Ok, could do better. But after years of brutal austerity and unprecedented bank debt, the little engine that is Ireland is still doing better than other peripheral countries. Take that Greece! Take that Portugal!

The report goes on though. GNP measure – not all that good; domestic demand measure – really not all that good. And then, well down in the story, in the seventh paragraph comes the bucket of water:

“GDP contracted in both the third and final quarters, by 1.1 and 0.2 per cent respectively. Two consecutive quarters of contracting GDP is the standard definition of an economy being in recession.”

I like that – by the standard definition we are in recession. By standard definition, you are unemployed (“Wow, so that's why I don't have a job”); by standard definition you are in poverty (“Hey, squire, got change for the bus?”); by standard definition you have emigrated (“I wondered why everyone was talking Dutch”).

The adjectives and metaphors come flying: “technical recession” and “an economy of two halves” – the latter referring to the fact that the economy grew in the first two quarters only to decline in the last two quarters.

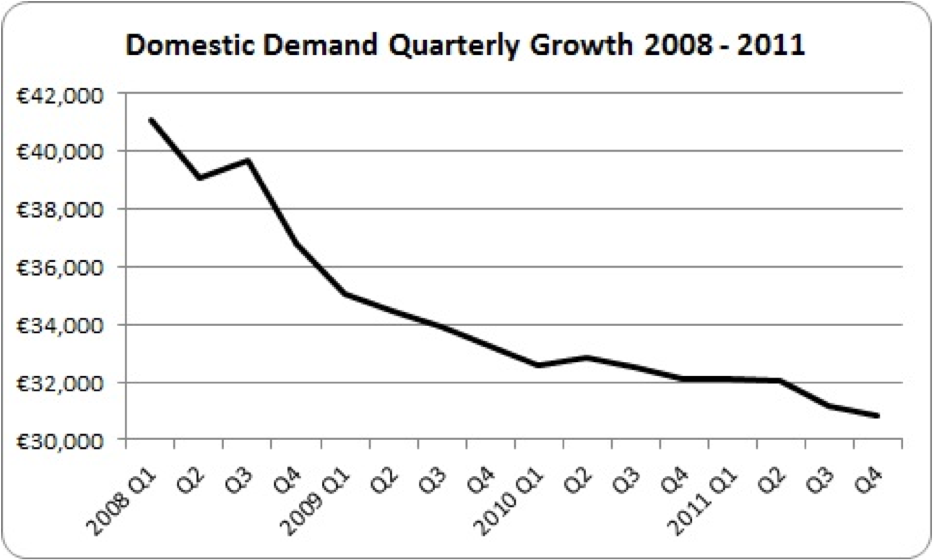

Let’s look at the larger picture. Irish economic data, always an Alice-in-Wonderland affair with multinational exports, profit-booking, transfer pricing and profit repatriation, still manages to tell the persistent story – a domestic slump that is continuing.

- Consumer spending fell by nearly 3% in 2011 – a much faster rate than the previous year

- Investment fell by nearly 11% – a slower rate than previous years but that’s only because it’s hard to see how investment could fall much further without completely disappearing (our investment rate is about half the Eurozone average)

- Government cuts in public services are still taking a toll on the economy

Some commentary has pointed to the slow-down in exports to explain this “economy of two halves”. Yet exports were higher – in both nominal and real terms – in the second half of the year than the first half. Ditto for net exports (exports minus imports). No, it’s not the export performance that has driven us into the standard definition of recession.

After flatlining for three quarters starting in late 2010, the decline in domestic demand resumed. There can be many explanations but a major one is Fianna Fáil’s last budget. Did anyone think that taking €6 billion out of the economy in regressive tax increases and spending cuts would have no effect on the domestic economy? Maybe it has no impact in Happy Land where we all live in gumdrop houses on Lollipop Lane. But in the real world it does have an impact – an inevitable and negative one.

In fact, the decline in domestic demand in the latter half of last year was the biggest two-quarter fall since late 2009.

So what can we expect in the short-term, given the last budget, which continued regressive tax increases and spending cuts? Here we have to look at runes:

- Consumer spending: the Retail Sales Index fell in January this year by the biggest monthly amount since January 2010

- Employment: the picture is mixed. There was a welcome increase in employment in the last quarter of 20l11 (though the jobless total still rose). However, the Department of Social Protection recorded a huge spike in redundancy notices in December 2011 – nearly 7,000. This was 70% higher than the previous 11 months. So it remains to be seen whether the employment increase recorded in the last quarter will be sustained.

- Exports: January figures for goods exports look positive – a 9% increase on the previous month, seasonally adjusted. The latest manufacturing PMI (Purchasing Manager Index) still remains in negative territory, however. The latest services PMI shows positive growth but still shows service companies shedding jobs.

Business insolvencies are still rising. Insolvency.ie reports that business insolvencies are up in the first two months of 2012 – 20% higher than the same period last year.

And we know that the Government will still continue to cut public services, though at a less brutal pace than the previous Government. This will continue to put downward pressure on economic growth.

So heading into 2012, the picture is mixed but in all likelihood we will continue to see a drain on domestic demand, partially compensated by exports – and potentially jobless export growth.

In all this we can only hope that Government ministers will start an open and honest dialogue with people. We need less “We’re marching towards recovery” and “the economy is ready to take off”. The fact is we’re, at best, flatlining, with data suggesting we still have a ways to go before domestic demand bottoms out. After all, we’re back in recession – however technical. {jathumbnailoff}

Image top: merwing little dear.