Normal business resumed on housing policy

Do we really believe that building and selling houses to each other is a pathway to recovery? The Government seems to think so. By Michael Taft.

There’s been a lot of discussion about whether 2012 will see property prices hit the ‘floor’. The Government and NAMA are doing their bit to help stimulate house purchases through budgetary measures and negative equity insurance schemes. Unfortunately, there has been little debate about the optimal level of house property prices. Few have been asking if it would be a good idea if property prices stopped falling this year.

A standard measurement of ‘house affordability’ is the ratio between median house prices and median household income. The authoritative Annual Demographia International Housing Affordability Survey suggests that affordability lies in the 3:1 range – median house prices should be three times or less the median household income. Anything above that threshold leads us into ‘unaffordability’ territory.

One of the problems is that we don’t have official data for these median components. So we have to patch this together. Conor McCabe has looked at the relationship between average house prices and average industrial wages and found that while the ratio hovered around the 4:1 mark between the mid-1980s and mid-1990s (that is, average house prices was four times the average industrial wage), by 2006 this ratio exceeded 11:1. Therefore, the ratio before the speculative boom can be considered the long-term sustainable ratio between house prices and wages.

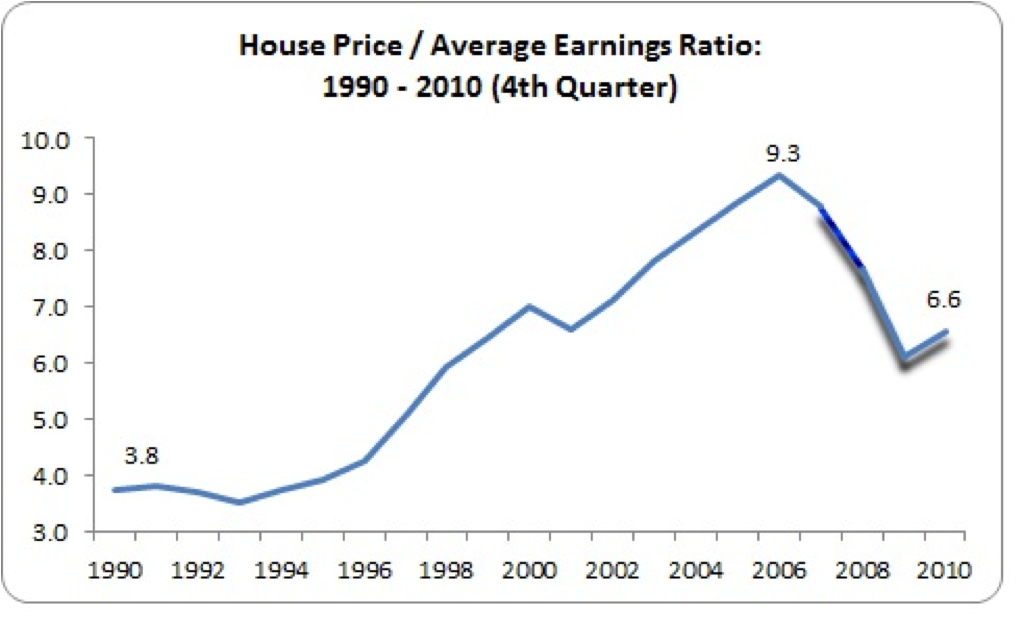

I have done my own calculation, using the Department of Environment data.

There are some minor differences with McCabe’s calculations (this data is based on manufacturing wages), but what both calculations show is the scale of the speculative boom. (The shaded area is my own estimate of wages, as the Department of Environment stops after 2007 because the CSO changed their wage calculation methodology.) They further show that pre-speculative prices fluctuated around 4:1.

There are some minor differences with McCabe’s calculations (this data is based on manufacturing wages), but what both calculations show is the scale of the speculative boom. (The shaded area is my own estimate of wages, as the Department of Environment stops after 2007 because the CSO changed their wage calculation methodology.) They further show that pre-speculative prices fluctuated around 4:1.

Ronan Lyons also looked at this issue and found that average house prices were about 3.6 times the average household income during the 1980s. Lyons suggests that this could be considered the equilibrium level. Back in July of last year he suggested that, using this 3.6:1 ratio, house prices needed to fall by about 25%.

So where does that leave us? In 2011, house prices fell by approximately 16%, which suggests that the ratio has fallen to something like 5.5. Ok, this is well below the speculative heights, but still well above that ratio of approximately 4:1 that pertained in the decade preceding the speculative boom. To get to that level, we need house prices to fall by another 25 and 30%.

Taking Ronan’s equilibrium of ratio of 3.6:1 we find that, using the EU Survey of Income and Living Conditions, house prices in 2009 were 4.3 times that of gross household income. This suggests a further fall of 16% is necessary – but we have to remember that gross household incomes are falling along with prices; so the fall in house prices would need to be more.

Ok, we have now been numbed by all these prices and ratios. What’s the bottom line? It should make us very worried that the Government and public agencies are pursuing policies to put a floor on prices. Housing costs – home-ownership and rents – should be driven down to a level of reasonable economic return, otherwise, they become a drain on the productive economy. If people have to spend more on housing themselves, they have less to spend in other sectors of the economy. This becomes a cost – and as we know from experience, a terrible cost; not only in diverting scarce resources from non-housing consumption, but through the danger of diverting investment away from productive activity.

What does it say about an economic policy that reviving a property market is considered desirable? Do we really believe that building and selling houses to each other is a pathway to recovery? Have we learned nothing? We are facing into a medium-term period of falling or stagnating real wages (wages after inflation) coupled with higher taxation that will reduce real disposable income. And we’re talking about reviving, or interrupting the fall in, property prices – especially when they are still well above their equilibrium?

Complex housing policies are reduced to one thing – property prices. We have rental accommodation issues (price, quality, tenants’ rights in a fragmented mom-and-pop sector); land prices and the Kenny Report; planning mechanisms for future land use; a potential regressive property tax; arrears and negative equity; rising homelessness; billions of euros available for individuals, companies and banks to cover their speculative losses in past years; degraded housing stock; local authority waiting lists; ghost estates; NAMA; a dysfunctional private housing sector and a quickly disappearing public housing sector, etc. etc.

But never mind all that. It’s all so very complicated. Let’s just talk about house prices. Let’s talk about “reviving the property sector”. Let’s continue to conflate the fortunes of the economy with the fortunes of the property market. We only need to focus on one index – and when it starts rising again, we’ll all feel so good about ourselves.

And normal business will have been restored. {jathumbnailoff}

Image top: topgold.