The Fiscal Treaty files: Will it cost us?

The Government and their austerity supporters have co-opted the language of progressives to avoid answering a fundamental question: what the cost of the Fiscal Treaty will be in terms of future austerity measures. By Michael Taft.

Will the Fiscal Treaty – in particular, the notorious structural deficit rule – require additional austerity? John McHale of the Fiscal Council says it won’t. He accepts that in 2015 the gap between the Department of Finance’s projected structural deficit (3.5%) and the Fiscal Treaty target (0.5%) is €5.4 billion. But then he argues that growth can wipe that deficit out:

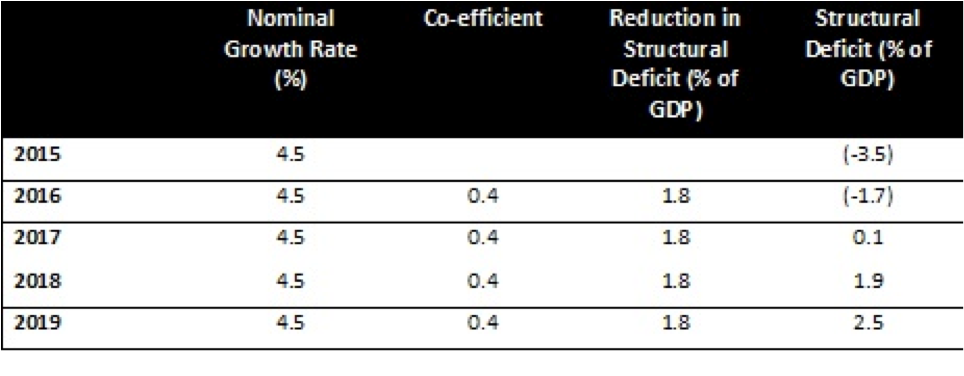

“Growth affects both the denominator and the numerator of the structural deficit as a share of GDP. (For simplicity I assume that actual and potential GDP grow at equal rates post 2015.) The denominator effect is straightforward. For the numerator, we could use the standard coefficient used by the European Commission for Ireland that assumes that the reduction in the deficit is 0.4 times the change in nominal GDP. (This coefficient is usually used for doing cyclical adjustments, but it should also be applicable for measuring the impact of changes in nominal potential GDP on structural balance in the absence of discretionary adjustments to tax and expenditure parameters.)”

On this basis John does some calculations – using a more conservative co-efficient of 0.2. He finds the structural deficit is effectively wiped out by 2019/2020 without any additional austerity, because growth has done all the heavy lifting.

I would suggest that this line of argument is flawed. First, I assume the co-efficient he uses refers to the cyclical sensitivity measurement of 0.4. This measurement is used to deconstruct the deficit into its ‘cyclical’ and ‘structural’ components. Essentially, you measure the gap between the real GDP and potential GDP growth and then apply the 0.4 to see how much of the gap is cyclical.

And herein lies the first problem – the 0.4 is an instrument to define the cyclical component of the output gap. It is not a measurement which defines the relationship between nominal growth rates and deficit reduction – whether it is the general or structural deficit. It is analogous to using a car clamp to change a light bulb. It is the wrong instrument. As the Department of Finance puts it:

“Indeed, by definition, reducing the structural element of the deficit will require policy action...”

The whole point of structural deficit measurements is to determine what the deficit will be when the economy returns to full capacity. If the economy is firing on all cylinders and there is still a deficit, then the Government must take policy action to correct this, because growth cannot.

In doing his calculations, John assumes that real and potential GDP grow at the same rate. Never mind that the Government estimates that real GDP is growing at twice the rate of potential GDP in 2015 (yes, I know, this suggests that the economy is ‘overheating’ – one of the absurdities with the model that the Department of Finance is using). If the output gap is zero, there is no role for applying the 0.4 co-efficient because there is no cyclical component to measure.

Seamus Coffey does his own calculations based on John’s more conservative co-efficient of 0.2 and applies it to GDP growth (though Seamus does say “There is no way of knowing” what this co-efficient is). He comes up with a similar result as John.

But there is a problem here. Why use a conservative 0.2 co-efficient? If you believe that 0.4 tells the story, go with it. And why, use a nominal growth rate of 3.5%? The Government claims that in 2015 the nominal growth rate is 4.5 percent. So let’s go with that.

What do we get? We find that the structural deficit turns into a structural surplus without doing anything.

And what a surplus! By 2019 we will have a structural surplus of 2.5%. We outdo even the Germans. We get to go to the top of the class.

And what a surplus! By 2019 we will have a structural surplus of 2.5%. We outdo even the Germans. We get to go to the top of the class.

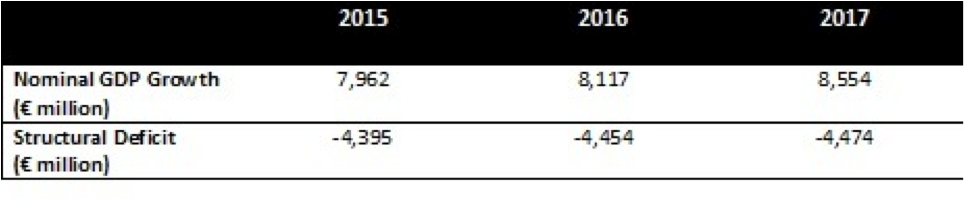

Is this likely? No. But we don’t have to argue the toss about cyclical sensitivity measurements or coefficients of elasticity. We merely have to go to the IMF’s own projection – which helps because (a) they stretch out to 2017 and (b) they assume, like John, no fiscal adjustment after 2015. What do they find?

In percentage terms, the reduction in the structural deficit is minimal: less than 0.1% of GDP each year.

In percentage terms, the reduction in the structural deficit is minimal: less than 0.1% of GDP each year.

But why should this surprise us? If there is deficit left over after the output gap is closed (after the economy returns to full capacity), what remains is the structural deficit which requires “policy action” to reduce it. (Of course, the very notion of a structural deficit is contested – to the extent that it is not very helpful at all in terms of sound fiscal policy as outlined here.)

Political implications

But there’s more to all this than just dueling statistics. The Government and their austerity supporters have co-opted the language of progressives to avoid answering a fundamental question: what the cost of the Fiscal Treaty will be in terms of future austerity measures. They are now talking about ‘growth’ being the main instrument of deficit-reduction. The Government has even gone so far as to say that investment will grow the productive capacity and, therefore, reduce the deficit. Some of us have been saying that since the start of the crisis – UNITE and the trade union movement, TASC, contributors on Progressive-Economy; all we got was ridicule and scorn.

Here’s how the Department of Finance puts it:

“Indeed, by definition, reducing the structural element of the deficit will require policy action, though not necessarily taxation and expenditure adjustments. Other options are available… Such measures include labour market reforms - some of which are already in train - together with investment in technology and infrastructure to boost the productive capacity of the economy. To this end, the Government has established NewERA and the Strategic Investment Fund…

This ambitious programme of microeconomic reforms, by boosting the productive capacity of the economy, is expected to help reduce the structural element of the deficit by the middle part of the decade. For example, reforms along the lines of those set out in the Action Plan for Jobs 2012 and the Pathways to Work initiative, aimed at addressing some of the skills mis-match in the labour market, should help lower the unemployment rate. This would have a structurally beneficial impact on the public finances, on both the revenue and expenditure sides. In other words, the structural fiscal position is set to improve with these microeconomic reforms.”

And, yet, yet – the Government still refuses to provide a projection for this. If they are convinced that investment and labour market reforms will boost our productivity, they can project this – through the ‘potential GDP’, which measures the contribution of labour, capital and productivity.

This is all a charade. At the same time as the Government is assuring us that growing our potential GDP will reduce the structural deficit, they are actually revising downwards potential GDP.

In the last budget, the Government projected that our productive capacity would grow by 3.4% between 2010 and 2015. Only a few months later, the Government is now projecting growth at 2.4%. This revision downwards reflects their lower GDP projections.

In the last budget, the Government projected that our productive capacity would grow by 3.4% between 2010 and 2015. Only a few months later, the Government is now projecting growth at 2.4%. This revision downwards reflects their lower GDP projections.

In other words, we are going forward by going backwards.

This is the ultimate game plan. Stonewall any questions about the cost of the Fiscal Treaty with talk of growing our productive capacity even as you revise downwards our productive capacity. ‘Prove’ that growth will reduce the structural deficit by using variables that have little reference to structural deficit reduction. But don’t ‘prove’ it too much because it will look nonsensical. Ignore what current projections (IMF) have to say about all this. Even ignore the definition of a structural deficit. Above all, abandon your austerity clothes and don the robes of an expansionary programme – even as you promise to cut public investment next year and cut spending on public services and social protection by even more than you did this year.

Do all this. But don’t call it austerity. {jathumbnailoff}

For more of our coverage of the Fiscal Treaty, click here.

For more of our coverage of the Fiscal Treaty, click here.