Do the EU and the IMF owe Ireland an apology?

The EU and the IMF have got it badly wrong in their predictions and projections for the Irish economy thus far. Time for them to own up to their mistakes. By Michael Taft.

There’s nothing wrong with saying, hey I got it wrong. We all get something wrong from time to time; never more so when the subject matter is economic and fiscal forecasting. When people and institutions don’t admit they got it wrong, especially when they got it demonstrably wrong, when the policies they are advocating are not hitting their target - that’s when cynicism and resentment arises.

So did the EU and the IMF get it wrong? There’s little doubt. The predictions and prognostications and statements of support are on the record – and they are way off target.

The basis of the EU-IMF bailout deal was the last Government’s National Recovery Plan (NRP), which was published only weeks before the bailout deal was sealed. According to the minister for finance at the time (December 2010):

“The [bailout] programme has adopted in its entirety the measures set out in the National Recovery Plan as a roadmap to return our economy to sustainable growth. The adjustment of €15 billion by 2014 has been accepted, as has the breakdown of €10 billion in spending reductions and €5 billion in revenue raising measures.”

When the bailout deal was signed, the EU and the IMF couldn’t say enough good things about the National Recovery Plan. They were positively ebullient and fully confident that this plan would work. It’s worth quoting in detail from the joint statement issued by EU Commissioner Ollie Rehn and IMF Managing Direct Dominique Strauss-Kahn:

“We strongly support the economic program announced today by Ireland . . .This program articulates a clear strategy for tackling today's problems and for harnessing the enormous growth potential of this open and dynamic economy. . . . It also offers a road map for sound public finances by setting strong, upfront actions in a multi-year framework...On the fiscal side, the program spells out both spending and revenue efforts over several years to repair the budget position...Carrying out this plan calls [for] a sustained effort by the Government and the people of Ireland. But it also offers a sound basis for stable, job-creating growth.”

This is quite a statement of support and affirmation. And it’s not like Ollie and Dominique were buying a pig-in-the-poke. The National Recovery Plan came complete with projections up to 2014 – economic and fiscal – which no doubt the experts at the EU and the IMF had gone over, examining every cell in every Excel worksheet. No doubt it passed their stress tests. Hence, the effusiveness of the EU and IMF’s support.

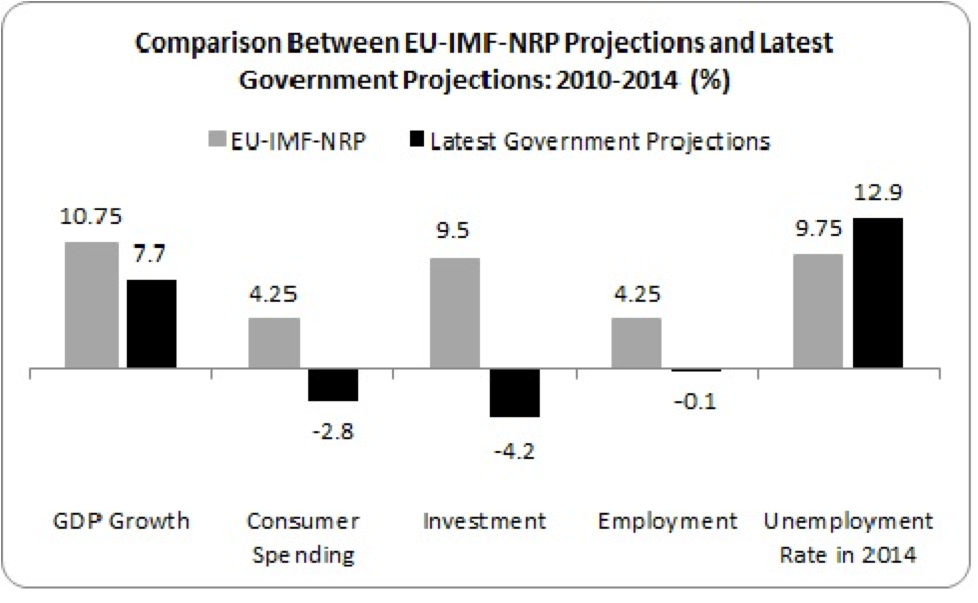

So how is the programme, based on the National Recovery Plan, faring? Not well. Let’s see how the projections are holding up, starting with the economic.

There’s going off-target and there’s going off-target. And then there’s this.

- GDP growth projections in the years 2011-2015 have been cut by nearly a third – with independent forecasters suggesting that 2012 is going to be even worse than the latest Government projections.

- Consumer spending: the EU-IMF-NRP estimated a modest increase but the latest projections are showing that it will be negative over the four years. Ouch.

- Investment: From a 9% increase to a -4% increase – that’s really wide of the mark.

- Employment: This is where it really goes off-target. The EU-IMF-NRP projections show employment increasing by over 4% – or nearly 80,000 jobs by 2014. The latest Government projections show employment actually falling, by nearly 2,000 jobs over the same period.

Now let’s turn to the fiscal or budgetary projections.

- Annual Deficit: the EU-IMF-NRP projections estimated the deficit to be 2.8% by 2014. The latest Government projection puts the deficit at 5%. This is partly explained by the extension of the target date for Maastricht compliance to 2015. This extension was necessary because the current Government found a €4 billion hole in the budgetary projections produced for the EU-IMF bailout deal only a few weeks after they came to office. I wonder if they discussed that with the Troika officials.

- Debt: the EU-IMF-NRP projections estimated the debt to be 100% of GDP by 2014. The latest Government projections estimate it to be 115% – and that’s after the €3.6 billion mistake.

- Cumulative Deficit: Over the four years, the General Government Deficit was estimated to be, in total, €41 billion in the years 2011-2015 (this doesn’t include bank recapitalisations). The latest Government projection is €50.2 billion. That’s over 20% off target only one year into the programme.

No matter how you rationalise this, it doesn’t look good – for the EU, the IMF or the Department of Finance. But as I said, everyone makes mistakes. The point is we should own up to those mistakes.

The officials from the EU and IMF are in town. Now would be a good time to start an open and honest conversation about the Irish economy, rather than hiding behind meaningless rhetoric and pep talks. It would be a great if an EU or IMF official walked up to the microphone and said:

“Sorry, but we got it wrong. We thought that the programme would work but it obviously isn’t. It’s not tackling today’s problems; it’s not bringing about job-creating growth. We need a new approach – a Plan B. We need a different debate about growth and jobs and debt. We need a new departure. Anyone got some ideas?”

Now that kind of honesty and humility would go down a treat. And if it takes a few months to work these new ideas into a coherent programme, that’s okay. Because there’s one thing for sure – this economy is stuck in a rut.

It ain’t going anywhere. {jathumbnailoff}

Image top: Bob.Fornal.