If a tree falls, does it make a sound?

David Vines and Max Watson say that Ireland's 'resilience' will see it through crisis. However, their analysis is more than a little light on facts, writes Michael Taft.

Gene Kerrigan is a litle dubious about claims of Ireland’s “unexpected economic recovery”. The article by David Vines and Max Watson of Oxford University, which first appeared in the Financial Times, went viral Irish-style, reprinted in the Irish Times and Independent and featuring on numerous current affairs programmes. And why not? They claim the markets have it wrong – that the Irish economy is on the path of recovery and that our ‘resilience’ will see us through. Ok, there are some challenges ahead (and we have to keep up that ol’ austerity) but if we persevere, we’ll make it to the sunrise.

Gene is right to be dubious. Others should be, too. Gene suggests that the Vines/Watson piece “seemed a bit light on facts”. Yes, there is that. Let’s look at some of these light facts that suggest economic recovery is on the way.

First, Vines/Watson claim we are “swiftly restoring our competitiveness” and, as proof, suggest that our current account surplus will soon be of the order of 3 to 4% of GDP. In other words, we will be exporting more than we are importing; selling more abroad than we are buying in from abroad. This is no bad thing, especially for a small open economy.

Our balance of payments has improved. In 2007 we had a deficit of approximately €10 billion. Last year it was €764 million in the black: not quite yet at 3 to 4% (more like ½%), but on the right track. Vines/Watson go on to say:

“Of course, recession has also played a role in turning external accounts around, but a steady uptrend in exports has been underway for some time.”

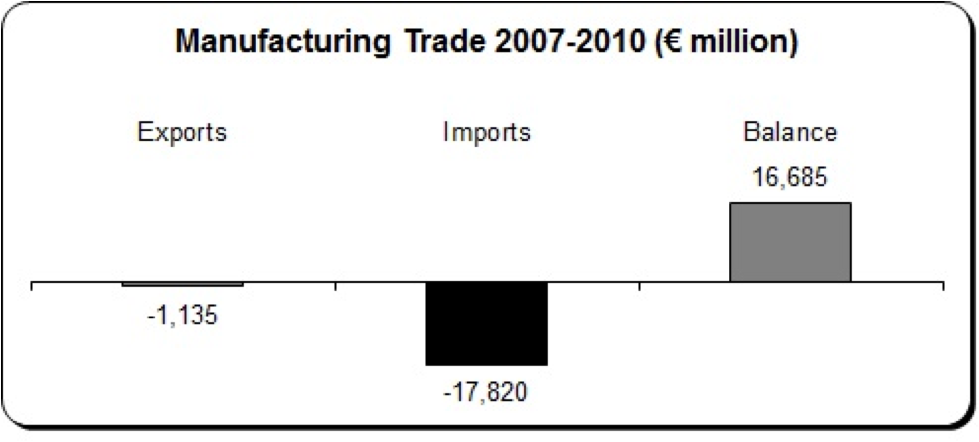

So which was it – recession or exports that turned the good ship balance-of-payments around? Mostly recession, actually. In 2007, our manufacturing goods trading balance was €19.8 billion; that is, we exported €19.8 billion more than we imported. By 2010, this balance shot up to €36.5 billion – quite an increase. What accounted for it?

We can see that the turnaround is all down, not to rising export earnings, but collapsing imports. Export value actually fell but goods imports collapsed by a phenomenal 28%.

Falling imports is about more than just household consumers too poor, too prudent or too nervous to spend. Most imports are bought in by businesses as inputs into their production or re-selling activities. Falling imports, especially of this magnitude, are a clear signal of an economy being gutted of business and household activity.

Second, Vines/Watson go on to discuss Ireland’s net public debt. They claim that it will top out at 110% – a high figure but not one that can't be overcome. Hopefully. But even topping out, we will still have the highest debt level in the Eurozone, bar Greece. It is hard to base an argument about ‘unexpected comebacks’ on the projection that we won't be as bad as the worst.

However, the following statement is simply bizarre:

“It is increasingly clear, too, that Ireland does not need to borrow from markets until 2014: that is the sort of borrower that markets can relearn to love.”

Imagine that you have been denied a loan from every bank in the land and you’re getting by on your in-laws’ generosity. Are you really someone that every bank in the land can relearn to love?

Third, Vines/Watson says our banking system is looking set to recover after the mega-billions of public subsidies. Hopefully. But there are three things to remember, even if these massive public subsidies manage to keep our banks afloat.

First, with the two main banks in active asset stripping mode, we shouldn’t expect too much credit flooding into the economy. Second, the investment into Bank of Ireland, which kept that bank from majority public control, could be seen as growing market confidence as suggested by Vines/Watson. Or it could be seen as a punt by investors who have a well-worked out risk portfolio. If the BOI investment doesn’t pay off, they haven’t lost much; but if it does they’ll cream it in. It may just represent a well-calculated bet, rather than anything to do with ‘confidence’.

Third, the investment community is not exactly rushing into AIB and and BOI yet. In March of this year, just before the latest recapitalisation was announced, their shares were trading at approximately 30 cents; now they’re trading at less than 10 cents.

So a balance-of-payments turnaround based on collapsing imports, a high public debt that is, at least, not as high as Greece, and growing confidence in our banking system, even with already low shares trading even lower: maybe Vines/Watson will turn out right – though this chart produced by Michael Burke should give us pause.

Or maybe Gene is right to be dubious. For if we are getting out of the woods, why are all these trees still falling on us? And do they make a sound?

And why doesn’t anyone hear them?

{jathumbnailoff}

Image top: cogdogblog.