Inequality: The real cause of the crisis

When it comes to official explanations of the current crisis, inequality is the elephant in the room. The report of the bipartisan US Financial Crisis Inquiry Commission, which blamed pretty well everybody and everything for the 2008 crash, failed to mention ‘inequality’ once in its mammoth 662 page report. Yet the historical evidence says otherwise.

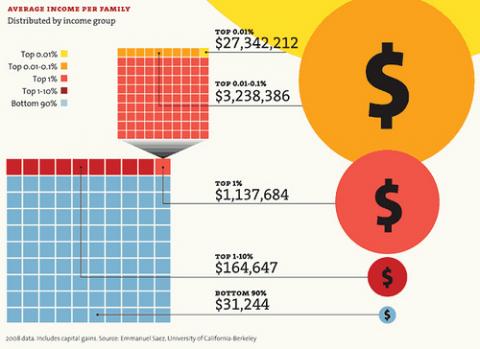

For the last thirty years, the gains from growth in a number of rich countries have gone increasingly to big business and a small financial elite. Since 1980, average real wages in the UK have risen at half the speed of growth, while in the US, living standards for four-fifths of the workforce have been little better than stagnant. In Germany the end of the party came a little later - real wages started flatlining from the millennium. It is these trends that have powered today’s towering personal fortunes, and left workforces with a declining share of the economic cake.

Yet the relationship between growth, wages and profits is critical to the course of economic stability. If wages rise more quickly than output, they cause inflation. If they fall too far behind they trigger recessions. It is no coincidence that the only period of sustained economic success of the last 100 years – the immediate post-war decades - was a time when wages and profits rose broadly in line with output. In contrast, the two most damaging recessions of the last century – in the 1930s and today – were both preceded by sharp rises in inequality, with wages falling increasingly behind growth.

In the United States in the 1920s, the share of income taken by the top 1% increased from 14 to 24%. From 1990 to 2007, there was a rise from 14.3% to 22.8%. There are two reasons why inequality – above a certain limit – leads to economic crisis. First, if the share of earnings in the economy falls sharply, as in the 1920s and the build-up to 2008, purchasing power does not keep pace with the extra output being produced. Consumer societies lose the capacity to consume. In both the 1920s and the 2000s, the demand gap was filled by an explosion in private debt. In both cases, this did not prevent recession, it just delayed it. Secondly, high levels of inequality eventually lead to asset price bubbles.

Wage change in the United States since 1979

In 1920s America, a rapid process of enrichment at the top fed years of speculative activity in property and the stock market. In the build-up to 2008, the rising corporate surpluses and burgeoning personal wealth that were the counterpart to the rising wage-output gap, led to a tsunami of hot money that merely created the asset bubbles – in property and business - that eventually brought the British and global economies to their knees. These lessons have yet to be learnt. In the UK, real wages are on a downward slide while corporate surpluses and personal fortunes are back to near record levels. It is this rising income divide that lies behind the faltering of recovery. Falling real earnings are stifling demand across the world’s richest economies. The globe’s billionaires and largest corporations are sitting on near-record volumes of cash, while the productive economy is being starved of funds.

Unless the imbalance between wages and output is corrected, we risk an era of near-permanent slump. {jathumbnailoff}

Stewart Lansley is the author of The Cost of Inequality: Three Decades of the Super-Rich and the Economy, Gibson Square.

Images: Mother Jones.